【学习笔记】-使用LSTM算法实现余额宝资金流入流出预测

发布时间:2024年01月21日

使用LSTM算法实现余额宝资金流入流出预测

关键词:LSTM、基于大规模历史数据预测、MSE

数据来源:[天池大赛-资金流入流出预测-挑战Baseline]

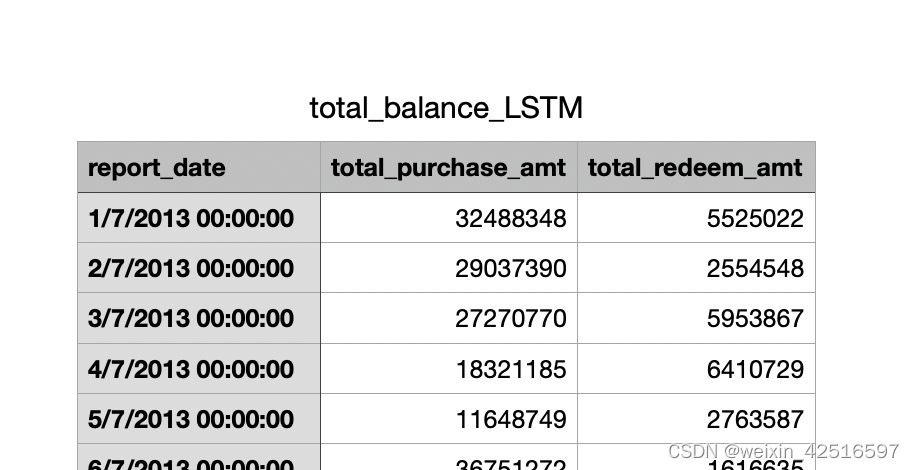

数据预处理:根据数据集进行数据预处理生成每日购入资金总量,最终传入的数据列表如下

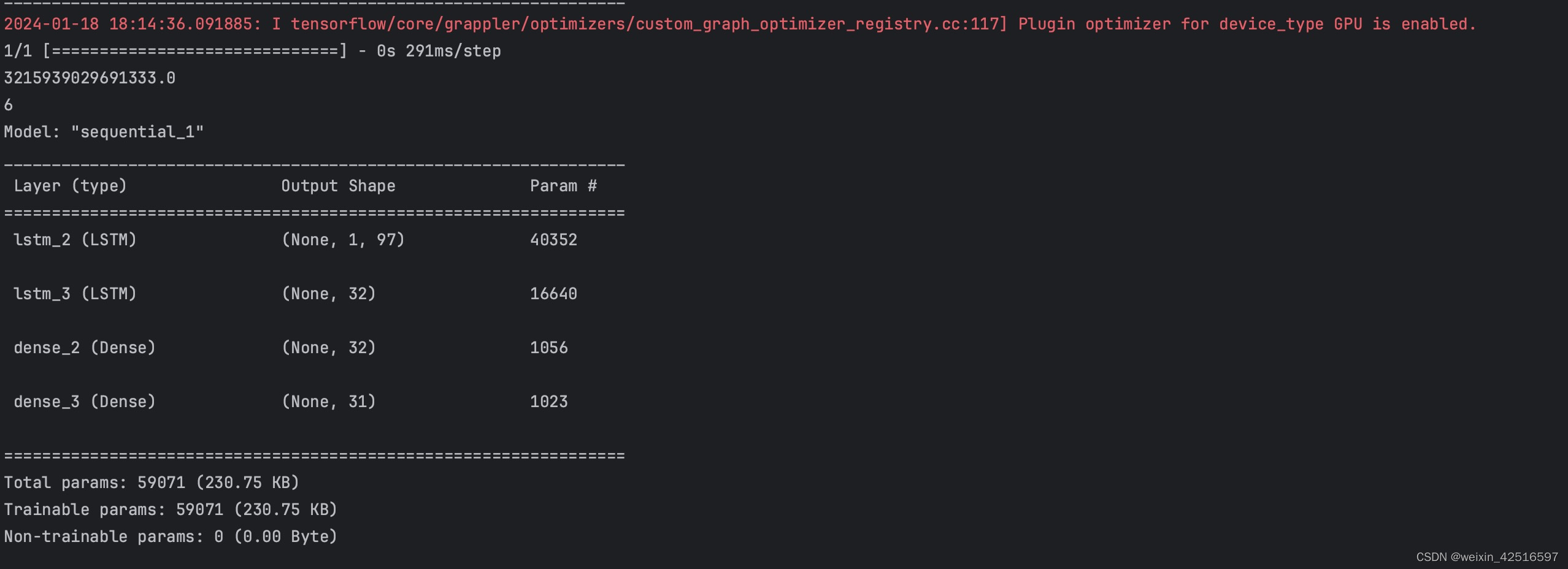

模型代码运行过程:

RNN模型运行数据

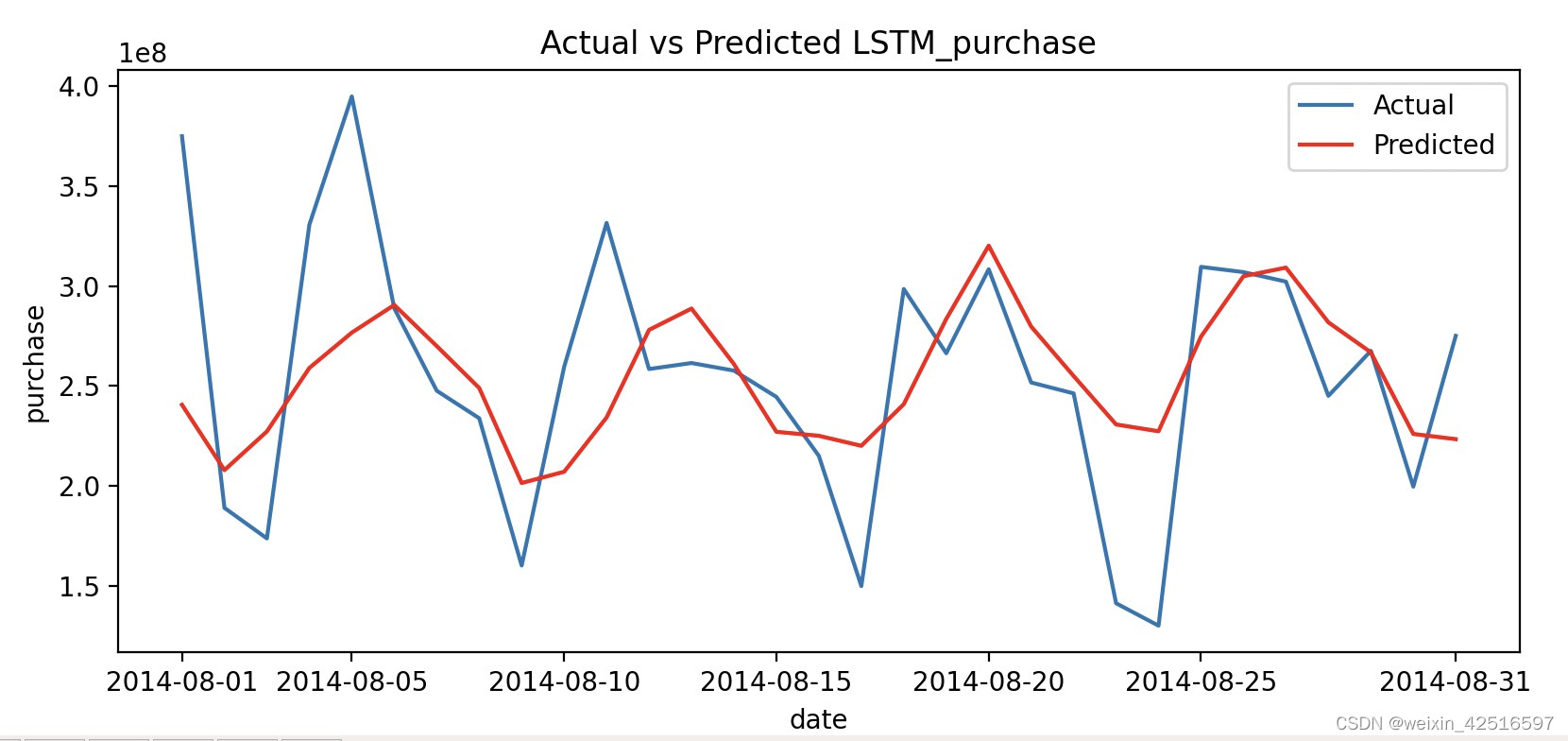

预测数据与原始数据对比图:

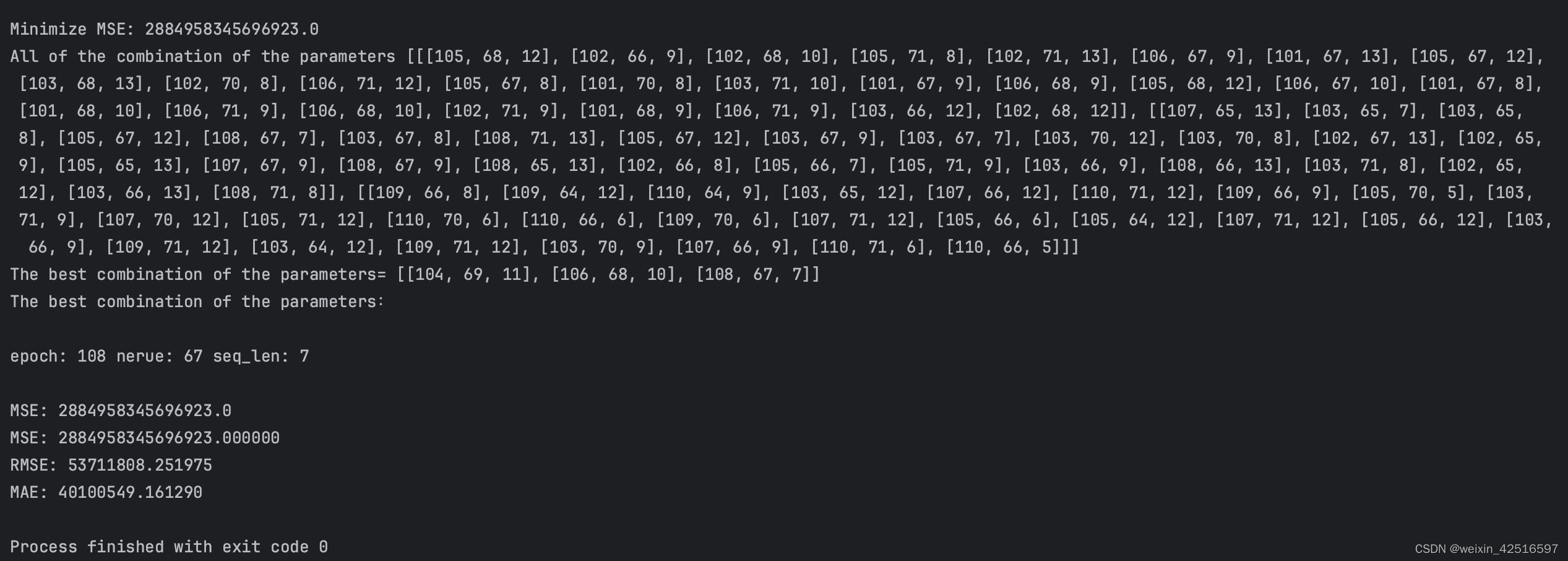

MSE、RMSE、MAE结果:

LSTM模型完整代码:

(数据量较大,代码运行时间较长,需要耐心等待)

#以下部分为项目需要引用的库

from math import sqrt

import numpy

import pandas

from keras.layers import LSTM

from keras.layers import Dense

from keras.callbacks import EarlyStopping

import matplotlib.pyplot as plt

from sklearn.metrics import mean_squared_error, mean_absolute_error

from random import choice

from sklearn.preprocessing import MinMaxScaler

from keras.models import Sequential

import warnings

warnings.filterwarnings('ignore')

#设置学习循环的次数(epoch)神经元个数(neure)步长(seq_len)的范围

numpy.random.seed(2019)

epoch_range=[*range(100,200,1)]

neure_range=[*range(10, 128, 1)]

seq_len_range=[*range(5, 50, 1)]

#定义参数组的list

List=[]

combination_all=[]

combination_best=[]

pred_best=[]

pred = []

epoch_best=None

neure_best=None

seq_len_best=None

MSE_best=399044410397529222

def Change_num(index_X,X_all_list):

if(3<=index_X<=(len(X_all_list)-3)):

list_X=X_all_list[index_X-3:index_X+2]

elif(index_X<3):

list_X=X_all_list[:5]

else:

list_X=X_all_list[-5:]

return list_X

#随机生成一组参数值

for i in range(0,1):

epoch=choice(epoch_range)

neure=choice(neure_range)

seq_len=choice(seq_len_range)

List.append(1)

List[i]=[epoch,neure,seq_len]

print(List)

leean=2

#RNN模型主体

class RNNModel(object):

def __init__(self, look_back=1, epochs_purchase=10, batch_size=1, verbose=2, patience=10,

store_result=False,nerue=1):

self.look_back = look_back

self.epochs_purchase = epochs_purchase

self.batch_size = batch_size

self.verbose = verbose

self.store_result = store_result

self.patience = patience

self.nerue = nerue

self.purchase = pandas.read_csv('/Users/Desktop/Purchase Redemption Data/total_balance_LSTM.csv', usecols=[1], engine='python')

#数据标准化

def get_Standard_data(self, data_frame):

# load the data set

data_set= data_frame.values

data_set = data_set.astype('float32')

scaler = MinMaxScaler(feature_range=(0, 1))

data_set = scaler.fit_transform(data_set)

train_x, train_y, test = self.create_data_set(data_set)

train_x = numpy.reshape(train_x, (train_x.shape[0], 1, train_x.shape[1]))

return train_x, train_y, test, scaler

def create_data_set(self, data_set):

data_x, data_y = [], []

print(self.look_back)

for i in range(len(data_set) - self.look_back - 31):

a = data_set[i:(i + self.look_back), 0]

data_x.append(a)

data_y.append(list(data_set[i + self.look_back: i + self.look_back + 31, 0]))

return numpy.array(data_x), numpy.array(data_y), data_set[-self.look_back:, 0].reshape(1, 1, self.look_back)

#LSTM模型主体

def LSTM_model(self, train_x, train_y, epochs, nerue):

model = Sequential()

model.add(LSTM(nerue, input_shape=(1, self.look_back),return_sequences=True))

model.add(LSTM(32, return_sequences=False))

model.add(Dense(32))

model.add(Dense(31))

model.compile(loss='mse', optimizer='adam')

model.summary()

early_stopping = EarlyStopping('loss', patience=self.patience)

history = model.fit(train_x, train_y, epochs=epochs, batch_size=self.batch_size, verbose=self.verbose,

callbacks=[early_stopping])

return model

def predict(self, model, data):

prediction = model.predict(data)

return prediction

#处理流入数据,划分训练集和测试集,并运行LSTM算法`在这里插入代码片`

def run_purchase(self):

purchase_train_x, purchase_train_y, purchase_test, purchase_scaler = self.get_Standard_data(self.purchase)

purchase_model = self.LSTM_model(purchase_train_x, purchase_train_y, self.epochs_purchase,self.nerue)

purchase_predict = self.predict(purchase_model, purchase_test)

purchase = purchase_scaler.inverse_transform(purchase_predict).reshape(31, 1)

test_user = pandas.DataFrame({'report_date': [20140800 + i for i in range(1, 32)]})

test_user['purchase'] = purchase

return test_user['purchase']

if __name__ == '__main__':

real = pandas.read_csv('/Users/Desktop/Purchase Redemption Data/total_balance_test.csv',usecols=[1], engine='python')

#抽取27组epoch、neure、seq_len的参数组合

for i in range(0, 27):

epoch = choice(epoch_range)

neure = choice(neure_range)

seq_len = choice(seq_len_range)

List.append(1)

List[i] = [epoch, neure, seq_len]

print(List)

leean = 2

for f in range(3):

MSE_list = []

pred_all = []

for s in range(27):

initiation = RNNModel(look_back=List[s][2], epochs_purchase=List[s][0], batch_size=14, verbose=0,

patience=50,

store_result=True,nerue=List[s][1])

prediction=initiation.run_purchase()

MSE_list.append(1)

MSE_list[s] = mean_squared_error(real, prediction)

print(MSE_list[s])

pred_all.append(1)

pred_all[s] = prediction

print(MSE_list)

indexs = MSE_list.index(min(MSE_list))

print(indexs)

pred_best.append(1)

pred_best[f] = pred_all[indexs]

epochs, neures, seq_lens = List[indexs][0], List[indexs][1], List[indexs][2]

combination_best.append(1)

combination_best[f] = [epochs, neures, seq_lens]

#计算不同参数的预测模型的预测结果的MSE值,根据MSE值选择最合适的参数组合

if (MSE_list[indexs] < MSE_best):

MSE_best = MSE_list[indexs]

epoch_best = epochs

neure_best = neures

seq_len_best = seq_lens

pred = pred_all[indexs]

print(pred[0])

index_epoch = epoch_range.index(epochs)

del epoch_range[index_epoch]

index_nerue = neure_range.index(neures)

del neure_range[index_nerue]

index_seq_len = seq_len_range.index(seq_lens)

del seq_len_range[index_seq_len]

epoch_new = Change_num(index_epoch, epoch_range)

neure_new = Change_num(index_nerue, neure_range)

seq_len_new = Change_num(index_seq_len, seq_len_range)

List = []

for y in range(27):

List.append(1)

List[y] = [choice(epoch_new), choice(neure_new), choice(seq_len_new)]

combination_all.append(1)

combination_all[f] = List

print(f, "th selection!\n")

print("epoch:", epoch_best, "nerue:", neure_best, "seq_len:", seq_len_best, "\n")

print("Minimize MSE:", MSE_best)

#输出预测结果最好的的最佳参数组合

print("All of the combination of the parameters", combination_all)

print("The best combination of the parameters=", combination_best)

print("The best combination of the parameters:\n")

print("epoch:", epoch_best, "nerue:", neure_best, "seq_len:", seq_len_best, "\n")

print("MSE:", MSE_best)

#绘制曲线图

plt.figure(figsize=(6, 4))

plt.plot(real, label='Actual')

plt.plot(pred, color='red', label='Predicted')

plt.xticks()

plt.title('Actual vs Predicted LSTM_purchase')

plt.xlabel('date')

plt.ylabel('purchase')

X=[0,4,9,14,19,24,30]

Y=['2014-08-01','2014-08-05','2014-08-10','2014-08-15','2014-08-20','2014-08-25','2014-08-31']

plt.xticks(X,Y)

plt.legend()

plt.show()

#输出预测结果的MSE、RMSE、MAE值

mseValue = mean_squared_error(real, pred)

rmseValue = sqrt(mean_squared_error(real, pred))

maeValue = mean_absolute_error(real, pred)

print('MSE: %.6f' % mseValue)

print('RMSE: %.6f' % rmseValue)

print('MAE: %.6f' % maeValue)

```

文章来源:https://blog.csdn.net/weixin_42516597/article/details/135680611

本文来自互联网用户投稿,该文观点仅代表作者本人,不代表本站立场。本站仅提供信息存储空间服务,不拥有所有权,不承担相关法律责任。 如若内容造成侵权/违法违规/事实不符,请联系我的编程经验分享网邮箱:chenni525@qq.com进行投诉反馈,一经查实,立即删除!

本文来自互联网用户投稿,该文观点仅代表作者本人,不代表本站立场。本站仅提供信息存储空间服务,不拥有所有权,不承担相关法律责任。 如若内容造成侵权/违法违规/事实不符,请联系我的编程经验分享网邮箱:chenni525@qq.com进行投诉反馈,一经查实,立即删除!

最新文章

- Python教程

- 深入理解 MySQL 中的 HAVING 关键字和聚合函数

- Qt之QChar编码(1)

- MyBatis入门基础篇

- 用Python脚本实现FFmpeg批量转换

- 暴雪意图复合,但国内已不是当年的市场

- 个人仿制android QQ、android大作业

- GPT如此火爆的几个重要原因

- 幻兽帕鲁服务器搭建,包教包会

- 软件测试|使用holidays模块处理节假日

- java8 Stream()流 list转map

- VOSviewer分析知网文献以及图片导出

- WTN6040F-8S语音芯片:投篮游戏机新时代引领者

- 使用numpy处理图片——90度旋转

- 【React系列】Hook(一)基本使用